A real story: how to correctly plan a family budget so that there is always enough money. In economy mode. How to learn to plan your personal budget

Why plan your family budget

The most important reason for planning is the conscious desire to get out of a lack of money. It's sad when the salary is decent, and you don't notice any special expenses, and the money disappears with the speed of the wind.

7 reasons why you should take the time to plan:

- This is how you estimate your family's monthly income. What's missing from the warehouse? What is not accounted for. If you know all budget receipts, then you can control these receipts.

- You will be able to identify the primary spending. Those items for which money goes first.

- Understanding how much money will be spent on basic expenses, and how much will remain on hand, will not allow you to make rash purchases (when they return after their paycheck with packages of new clothes, and spend the rest of the month on starvation rations).

- You will be able to identify important long-term goals and go towards them. Don't complain in the abstract – I want a new phone, car, apartment, but save it for the right purchase.

- Life is unpredictable. If you've budgeted a financial cushion for contingencies, you can handle them without compromising your entire budget. You don't have to ask for a loan and eat pasta until the paycheck.

- If you write down all the recurring expenses, then prepare for them in advance.

- Planning is not a Spartan infringement of one's own interests, it is insurance against unforeseen expenses and a kind of antidepressant (control over finances, the understanding that you have money in your bins for a rainy day is quite good at reassuring).

We offer an algorithm on how to distribute the family budget for a month in tables step by step:

There are 3 types of family budget

Traditionally, the family budget is divided into 3 types:

- General – this means that in a pair there is no separation of funds into “mine” and “yours.” All 100% of their income is added to the “one pot”. The general budget is more suitable for couples who have been living together for more than one year, as well as families with children and couples where one of the spouses earns significantly more than the other. Each spouse has the same access to money and the equal right to dispose of it. But here it can be difficult to choose gifts for each other. Also, with such a budget, it is necessary to negotiate all expenses (both large and small), and spontaneous purchases can cause disagreements.

- Separate – everyone disposes of their earned money as they wish, without discussing spending with a partner. And the total costs are divided either in half or by agreement. Such a budget is typical for couples who do not live together or have just moved in and are just starting to live together. The advantages of such budget management are financially independent from each other: everyone is responsible only for their own expenses and income. And the disadvantages are that there can be disagreements and even conflicts in spending on common needs.

- Mixed – when everyone saves part of their own earned money for general family needs, and leaves a part for personal expenses. Here the agreement of partners is important: joint funds can be spent only on the agreed things, and personal money – at your own discretion. This type of budget is suitable for couples where both spouses have a stable income and live together. The main plus here is the financial independence of each spouse. But this kind of budget needs regular monitoring and “data optimization” at least a couple of times a year.

What is planning, how to do it, so as not to get bogged down in papers and checks?

Planning is a series of sequential actions that must be carried out – each at its own stage. Nothing can be missed, otherwise the whole chain loses its meaning, which we observe everywhere.

Today, you do not need to bury yourself in papers and checks, everything can be done electronically. Unfortunately, most of the applications that are now on smartphones are not suitable for correct financial accounting. I know only 2 applications that I recommend to my clients, and which are more or less suitable for this task – Smart budget (for iPhones) and Zen-money (for iPhones and Androids). Plus, I additionally offer an Excel spreadsheet that is configured to automatically process data from these applications and analyze it on a monthly basis.

What are the planning stages:

- creating a plan for the year in the context of each month and by categories of income and expenses, necessarily fixing balance sheet positions;

- input and accounting of actual income and expenses, movement of funds (that is, you do not spend randomly and spontaneously, but check and focus on your plan);

- then you must bring the balances at the end of the month (the calculated balance corresponds to the actual balance that is on each account);

- then there is a comparison of the plan with the fact (analyze how you fit into your plan, why you planned something incorrectly, maybe you forgot about some expense or income or did not follow this plan);

- adjusting the next month and tracking how these changes affect your bottom line for the year.

What indicators should be recorded?

It is worth fixing:

- account balances – how much money you have available;

- your debts – how much you owe, to whom, when, if it is an official loan from the bank – how much you pay for your debts monthly, how much you pay in total;

- it is imperative to fix the amount of capital – this is the main indicator of your financial condition;

- income and expenses.

It is also important to look at the end of the month result – profit / loss. That is, evaluate whether you have a positive balance or a negative one. Your capital is increased by a positive balance, which is obtained at the end of each month. If it is negative, you spend more than you earned, which means that you either “eat up” the previously accumulated capital, if there is one, or you are forced to go into debt.

How to properly distribute the family budget

A few of the rules of thumb for family budgeting, which we will present here, can serve as a rough guide for decision-making. Everyone's situation is different and constantly changing, but the basic principles will serve as a good starting point.

The 50/20/30 rule

Elizabeth and Amelia Warren, authors of All Your Worth: The Ultimate Lifetime Money Plan, describe a simple yet effective way to budget.

Rather than breaking down household spending into 20 different categories, they recommend dividing the budget structure into three main components:

- 50% of income must cover basic expenses such as paying for housing, taxes and buying groceries;

- 30% – optional expenses: entertainment, going to a cafe, cinema, etc .;

- 20% goes to pay off loans and debts, and is also set aside as a reserve.

The 80/20 rule

80 to 20 or Pareto Rule – A variation of the previous rule. 20% of all income in the family budget to use to pay debts and create a financial “pillow”, 80% – everything else.

These rules of thumb can and should be adjusted to match your actual situation. Below you will find an example of a family budget in the table, which will serve as the basis for drawing up your own plan.

Rule 3 – 6 months

You must have on hand or a deposit sufficient for the family to live for three to six months. In the event of dismissal, accident or illness, the “safety net” will keep you from making desperate decisions, will give you the opportunity to look back and find ways out of the current circumstances.

The seven-envelope rule

On the forums about the problems of personal finance, many experts speak positively about the application of the “7 envelope rule” and give advice on how to properly use this method of family budgeting.

The rule of “7 envelopes” is to immediately distribute the amount of income for 7 envelopes on the day of receipt of the salary according to the main items of expenditure:

- obligatory payments;

- costs for children;

- funds for food;

- money to buy things, furniture, household appliances;

- money for family vacations, entertainment, vacations;

- accumulation;

- “Joy” – money left over from the previous month after the obligatory spending.

- In the first envelope – “mandatory payments” – the amount of money required to pay utility bills, mobile communications, the Internet, and repayment of a loan is set aside. The sum of these costs is more or less stable, but even here there is an opportunity to save a little by installing meters and reasonably reducing the consumption of electricity, gas, and water.

- In the second envelope, the money provided for the maintenance of children is deposited: payment for kindergarten, school fees, circles, sections, tutors. It is also necessary to provide money for the purchase of children's clothing, shoes, toys, etc. You can reduce the spending of the family budget on this article by taking advantage of sales in chain stores, on Internet sites, and the services of intermediaries in groups of joint purchases.

- The third is funds for food. You can understand how much a family needs for a month using the method of calculating expenses within 1-3 months. In today's conditions, at least 30-50% of the family budget is spent on food, these expenses must be strictly controlled, because there are many temptations to spend money on all sorts of “snacks” and go beyond the budget. To save money, experienced housewives advise using various promotions that are held in stores, you can find out about them in advance on specialized sites. Purchase of several packs of quality tea, coffee for the promotion will reduce spending on these products next month.

- Fourth – “things”: clothes, shoes for adult family members, household appliances, furniture, interior items. It is recommended to calculate a monthly approximate plan for the acquisition of these things, based on the total family income, their cost and the need for the family.

- In the fifth envelope money is put aside for family entertainment and recreation. The amount may vary depending on the availability of birthdays of family members in a particular month, planned trips to leisure centers, pizzerias, restaurants.

- The sixth is “accumulation”. A certain percentage of the amount of income should be set aside in it, but not less than 10%. This money is an emergency reserve, if suddenly there is a need to take some amount from this envelope, you should replenish it as soon as possible. The savings can be used to purchase a large purchase.

- The seventh envelope is “joy”. This is the money that was left after the obligatory spending from the previous month. They can be spent on nice gifts for family and friends.

The “7 envelopes” system works only if you strictly adhere to the limits of the allocated amounts for certain needs and never take money for the allocated categories of expenses from other envelopes.

Step 1. Determine sources of income

To determine the source of income, they find out permanent and periodic income, how much they constitute from the entire budget, what source of income works without your participation.

Basic income

The main income is the basis for building a family budget. Most of the main income is wages. It is stable, periodic, and it is convenient to plan on its basis.

Additional income

We add to the additional income:

- periodic part-time jobs;

- interest on deposits;

- cashback;

- awards;

- rental income.

Volatile income

Variable income should not be included in the general budget. Tax deductions are a visual item of volatile income. Put it aside in a piggy bank right away, form a financial security fund. Or start up to pay off large loan debts.

Step number 2 – How to distribute the family budget

First of all, we take permanent income and subtract 5-10% from them – who is more comfortable.

This is done in order to create a stock for a rainy day. So that in case of unforeseen expenses, money was where to get it

If you lack the discipline to save money on your own, then use the goals in Sberbank-online (as an example, other banks also have a similar tool).

Arguments AGAINST saving money (misconceptions)

- there is no money left at all, there is nothing to save, I live from paycheck to paycheck

- the amount is too small, there will be no sense from it

- inflation will gobble up everything

Arguments FOR saving money (reality)

- Utilities payments will grow by 5% tomorrow. What are you going to do? Will you find the money or will you stop paying?

- Suddenly, a tooth aches and urgently needs treatment, but there are not even 2-3 thousand rubles in stocks. Trifle? Yes. But, sometimes, even such a trifle can be very useful.

- What is better than 0 rubles or 5000 rubles in your pocket? I think the answer is obvious, even if in a couple of years these 5000 will cost less, but they will also be better than nothing.

We break all expenses into categories

mandatory expenses that cannot be reduced (mortgage payments, utilities, tuition fees, etc.)

mandatory expenses that cannot be reduced (mortgage payments, utilities, tuition fees, etc.)- mandatory expenses that can be reduced (food, car, etc.)

- non-obligatory expenses that can be waived without much damage (going to the gym, some kind of entertainment, etc.)

We get groups of expenses sorted by priority. If expenses from the third group can be skipped, from the second – to reduce, then with the first group it is difficult to do anything.

Accordingly, we distribute the family budget for a month based on the priorities received:

- first we allocate money for the first group

- then the second

- if something remains, then select it in the third.

In this way, you can distribute the family budget for a month.

Income – 20,000 rubles.

We put aside 5% for a rainy day – that's 1,000 rubles.

The remaining 19,000 rubles are divided into categories.

Let the communal apartment be 4,000 rubles, 6,000 rubles for food, 1,500 rubles for clothes, 1,500 rubles for travel, 2,000 rubles for health, 1,000 rubles for rest, 1,000 rubles for households. goods, and distribute another 2,000 rubles yourself.

It will also be useful to read the article – How to live on a small salary?

But that's not all.

It is not enough to distribute money, you still need to control how it is spent. This will ultimately save the family budget.

3 tips for making it easier to control costs:

- Compile a file in Excel with all income and expenses and fill it out every day (a selection of programs and services for maintaining a family budget).

- After a certain amount of money has been allocated for each category, you need to divide it into 4 weeks. On a shorter time frame, it is easier to keep track of when a category's budget is approaching the designated boundary and cut costs so as not to go out of bounds.

- It is best to write down expenses every day and not rely on your memory.

Immediately I foresee an objection:

“Why write down expenses every day, if we have already allocated where and how much we will spend? And so I remember! “

An example from personal experience

Although the expenses are of the same type, it happens that I get lost and start remembering at the end of the week how much and where I spent. As a result, up to 20% of the allocated budget of other categories has to be recorded in the category of ” unaccounted for ” (I am bringing in those expenses that I cannot remember where I spent, so that there are no inaccuracies).

20% is a significant discrepancy

And one more thing, I have been keeping track of expenses for the fourth year already, so I know how much and when I spent money. This information is very useful if you want to save money because it becomes clear where you can reduce costs or predict spending.

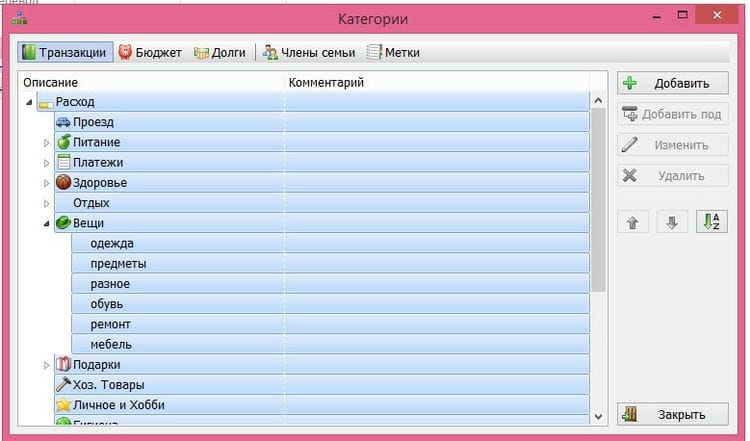

Step number 3 – Table of the family budget with expenses for the month

It is convenient to take intervals of a week, month and year. The weekly and monthly intervals allow you to control running costs, and the annual interval allows you to take into account non-fixed costs (holidays, birthdays, vacations, etc.).

2 principles of adding cost categories:

- there are expenses for which we want to track – we single out them in a separate category

- we want to get detailed information – we divide categories into subcategories

Below is a detailed table of costs.

Food

|

If desired, the data under categories should be broken down in even more detail (vegetables, meat, drinks, etc.) – this will allow you to assess which foods need to be reduced in the diet, and which ones would be better added. |

Payments

|

I think everything is clear here. Now it is easy to say exactly how much the cost of certain services has grown. |

Loans

|

|

Travel

|

|

Car

|

This category is taken out separately, since it is an essential part. Records of this kind will show you exactly how much the maintenance of the car costs, and from the link you can estimate approximately. |

Purchases

|

This should not include large categories such as car. |

| Household. Products | Every little thing: light bulbs, hooks, clothespins, etc. |

| Hygiene | Soap, shampoos, washcloths, etc. should be added here. |

Health

|

A large category that is also worth watching more closely. |

Presents

|

Split into subcategories: names of people, names of holidays. |

| Hobby | Here I think everything is also clear. |

Relaxation

|

|

Vacation

|

I took it out separately, since this is also a fairly voluminous category of expenses that is useful to track. For example, last year you went to China and recorded all expenses. If you decide to repeat the trip this year, then you will already have some kind of landmark. |

Repairs

|

It is also useful enough to write down expenses so that it will be easier to plan this kind of work in the future. For example, how much did it cost me to renovate a one-room apartment with a rough finish. Even after a few years, it will not be difficult to count everything. |

| Training | Also, if necessary, split into sub-items. |

| Debts | Enter data here when you borrow money to someone. |

| Not accounted for | At times, it becomes too lazy to keep track of expenses on a daily basis, so gaps that need to be written off somewhere are inevitable. You can use this solution. |

A table with expenses has been drawn up. If there is no category, then add it.

Step # 4 – Create a Financial Safety Cushion

Once again I will draw your attention to these points.

Financial safety cushion – if there is no money in reserve, then you can get into a difficult situation – this is a risk.

Therefore, first of all, 5-10% of the salary should be directed to creating a reserve that will allow you to live without any sources of income. A stock for a couple of months will allow you to survive the dismissal, a stock for half a year will allow you to survive a protracted illness.

- Financial independence – additional income can be spent on entertainment / shopping or deposited in a bank account. A more convenient tool is the Tinkoff Black debit card.

- Alternative to deposits – Individual investment account (there are some nuances).

Family planning and budget management

After you've fixed your expenses for a month, two or three months, it's time to start planning and more consciously managing your family budget.

The result of your planning should be a deficit-free budget. That is, your income fully covers your expenses. Ideally, there is still free money that you can send to the investment part of the budget.

There are three principles that will help you plan and manage your home bookkeeping properly, as well as help accelerate the achievement of financial independence.

- Your income should always be more than your expenses.

- The growth in income should be higher than the growth in expenses.

- The money saved should be directed to the investment fund.

First of all, you need to determine the exact size of each expense item in your budget. And in no case go beyond its limits during the month. If necessary – save! This is a great opportunity to develop this quality of rich people in yourself.

Fix the size of expense items for a year, and during this year do not increase their size unless urgently needed. At the very least, do your best for this. Review your expenses and related items quarterly.

We advise you from the items of regular spending, on which money should not be saved, to transfer the saved funds to items in the investment fund on a monthly basis. This will significantly increase the rate of accumulation of money for investments.

When working with the revenue side of the budget, you need to focus on increasing its residual side, and not on increasing wages. Since, when you concentrate efforts on increasing the share of wages in the income part, and in case of job loss, the income part will shrink more significantly than if you increased the residual part. After all, it does not depend on whether you go to work or not. Strive to ensure that this portion fully covers your monthly expenses.

You can distribute money by items of expenditure either at the time of receipt of funds by income items, or at the beginning of the month. This will turn out to be a kind of lending to your budget, the main thing is to make sure that income and expenses come together at the end of the month.

So for a more detailed analysis of spending, specialized applications are suitable. For example, Getcoin or Edadil. The most interesting functionality of these applications is downloading receipts and their subsequent analysis by type of purchases.

For example, after shopping at grocery stores, you upload all receipts to the app. And you do this for a month. After analyzing the information received, you will be able to understand what products and how much you spent, and then make an informed decision on optimizing costs.

You may find that you spend a lot of money on sweets. Maybe you should reconsider these costs? After all, reducing sugar consumption will have a positive effect on your health and the health of your loved ones.

One of the solutions to simplify the accounting of your daily expenses will be the transition to the use of bank cards. Since all banks have their own applications, which, in addition to storing the history of your expenses, provide analytical information on expenses by category. And it's completely free.

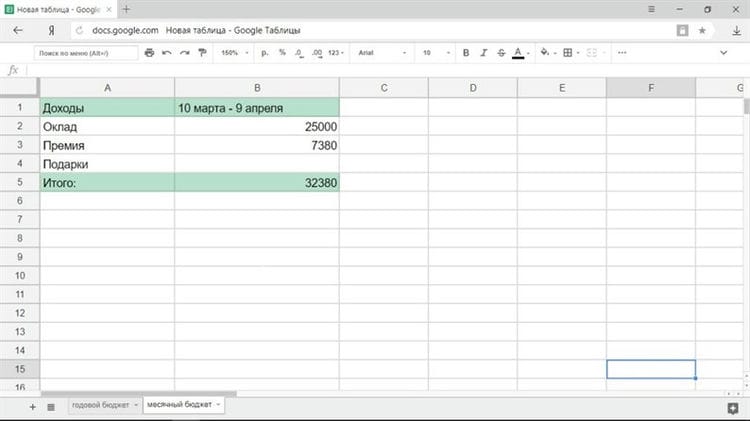

How to budget for a month

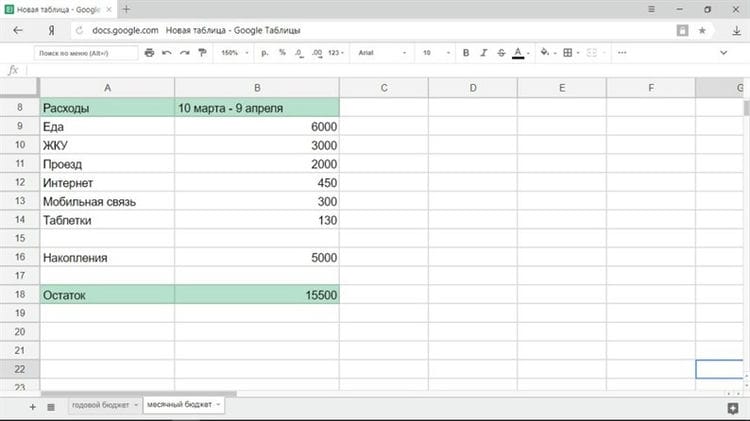

As a rule, the main part of the salary is not paid on the first day of the month, but on the 5th, 10th or 15th. Therefore, it will be more convenient to plan a budget not for a calendar month, but for the period from paycheck to paycheck, for example, from March 10 to April 9.

Income

First, you need to record all financial receipts in order to understand how much you have at your disposal. All sources of income should be taken into account: salary, bonuses, part-time jobs, money from renting an apartment, and so on. In case of unstable earnings, it makes sense to form a budget when you will know exactly how much you have, for example, on the day the money is credited to the card.

Costs

The first items of expenditure should be entered, without which you cannot do anything. This list will look something like this:

- Groceries (including lunch at work if you eat in the cafeteria).

- Communal payments.

- Directions.

- Mobile connection.

- The Internet.

- Household chemicals.

Naturally, the list of mandatory payments will be different for each person and for each family. The fare can be replaced by the cost of gasoline. People with chronic illnesses will consider spending on medications. The same list will include loan payments, a kindergarten fee, and so on. In this case, the traditional trip to the cinema on Saturdays and similar items of expenditure are not required.

Make it a rule to save money in a “stabilization fund” every month. This can be a fixed amount or a percentage of income.

The amount remaining after the deduction of mandatory expenses can be accessed in two ways:

- You distribute money for entertainment, clothing, and other amenities.

- You divide the remaining amount by the number of days in the month.

With the first method, everything is clear: you determine that you will spend 3,000 rubles on a movie, the same amount on clothes, and so on. The second method is worth considering in more detail.

Let's say you have 15,500 rubles left, and there are 31 days in a month. This means that you can spend 500 rubles daily. At the same time, the obligatory expenses have already been taken into account in the budget, so this money is calculated only for pleasant spending or force majeure. Accordingly, if you spend more than this amount per day, then you go into negative territory, and at the end of the month you will have to tighten your belt tighter. If you do not spend anything, then within two weeks, save 7,000 rubles, which can be spent on something big.

The money remaining at the end of the financial period can be spent or postponed. The first way is pleasant, the second is rational.

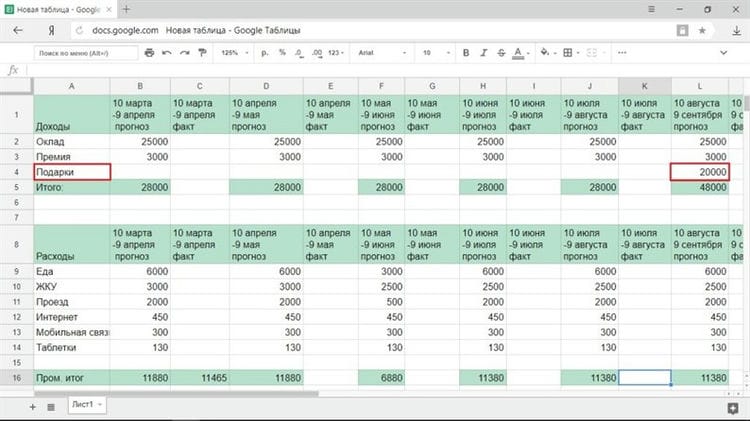

How to plan your budget for the year

The annual financial plan will need to be regularly adjusted for both expenses and income, so all columns in it need to be created in duplicate: the forecast and the actual indicator.

If you have a steady income

With a fixed amount of earnings, you simply enter the salary and other stable income in the income section. The only thing that will interrupt the usual course of things is vacation pay. Usually, before the vacation, they give money for the days during which you will rest, but then you will miss a certain amount in your salary. But in general, at the forecast stage, especially if you are making a budget for the first time, it will be enough to use only the salary for all months.

If you have a fickle income

With irregular receipts, there are three ways to forecast income:

1 You are sure that you will receive a monthly amount sufficient for living, although you do not know its exact amount.

Calculate your average income and use it to calculate. If you earn more than the projected amount in any month, move the excess to the piggy bank. You will get into it if you earn less than average.

2 You do not have a permanent income, and you are not sure what will happen.

It is better to take the minimum income as the basis for calculations. In this case, budget planning will become an asterisk problem, but there will be no financial surprises either.

3 Part of your income is stable, but it is difficult to predict the exact amount of earnings.

For example, you receive a fixed salary, and the availability of a bonus depends on many factors. Then it is worth planning the budget so that a stable income covers all the primary needs, and you will spend on the rest according to the situation.

Do not forget to take into account the income that you receive irregularly: quarterly bonus (every three months), tax refund (once a year), and so on.

For example, let's take a situation where most of the income is stable – this is a salary. The minimum premium is 3,000 rubles, and we will use this figure in our forecast. We also note that for the anniversary in August, they must give at least 20,000 rubles: parents promised 15,000, friends will surely give at least 5,000.

How to properly plan a family budget in the table

Now you know what is really going on with your money.

Take a look at the categories of expenses that you want to cut and create your own plan using the free excel spreadsheet.

Many people do not like the word “budget” because they believe that it is – restrictions, deprivation and lack of entertainment. Relax, a personalized spending plan will allow you to live within your means, avoid stress and sleep better, rather than pondering how to get out of debt.

Make sure the balance total is positive or zero before moving on.

“An annual income of £ 20 and an annual expense of £ 19.06 leads to happiness. An income of £ 20 and an expense of £ 20.6 lead to suffering, “Charles Dickens's ingenious note reveals the basic law of planning.

Enter your finished family budget into a spreadsheet

You set goals, identified income and expenses, decided how much to save each month for emergencies, and figured out the difference between needs and wants. Take another look at the budget sheet in the spreadsheet and fill in the empty columns.

The budget is not static figures fixed once and for all. You can always correct it if necessary. For example, you planned to spend 15 thousand monthly on products, but after a couple of months you noticed that you are spending only 14 thousand. Add additions to the table – redirect the saved amount to the “savings” column.

How to plan a budget with irregular income

Not everyone has a full-time job with regular salary payments. This does not mean that you cannot create a budget; but that means you have to plan in more detail.

- One strategy is to calculate the average income over the past few years and target that figure.

- The second way is to determine for yourself a stable salary from your own income – what you will live on, and put the surplus on an insurance account. In lean months, the account balance will decrease by exactly the missing amount. But your “salary” will remain unchanged.

- The third planning option is to maintain two budget tables in parallel: for “good” and “bad” months. It is somewhat more complicated, but nothing is impossible. The danger that lies in wait for you along the way: people spend and take out loans, expecting income from the best months. If the black streak drags on a bit, the funnel will eat up both current and future income.

Barn book or where to keep a budget

Anyone who asks the question of managing a family or personal budget is not changed faces a dilemma: where to keep the budget? In a notebook or Excel or a specialized program?

Each method has its own pros and cons. The main thing is to start keeping a budget, develop a habit of keeping it on a daily basis, and only then you will understand which tool is best for you.

It is important that in the selected tool you can plan your budget for a month, a year and enter data on actual expenses. And also it was possible to keep track of bank accounts and other financial instruments and flexibly customize them for your tasks. After all, it is important not only to take into account your expenses, but you also need to manage your saved monetary resources.

cost accounting

Programs and online services

At the initial stage, for someone, it will be easier to use a specialized program or online service (specify a list of programs), since you can record your expenses immediately at the time they are committed and begin to form the habit of keeping the family budget. Just select an app with multiplayer support. So that you and your half can keep track of expenses.

The advantages of this tool include portability, simplicity and clarity. You can easily generate graphical reports of your budget.

The disadvantages of using applications include the fact that most of them are paid, at least if you need more advanced functionality or the number of users. Plus, it can be very difficult to customize them for your specific tasks, especially in the free version. And they (specific tasks) will surely appear as you manage your family budget and develop your financial literacy.

For example, you start investing in real estate and you will have objects that will generate income and you will need to keep financial records on them. Keep in mind that you need to separate the family budget and the business budget.

Or you will need to keep track of the budget of a specific expense item in different banks. And many other individual tasks.

Excel or Excel or Excel – the main result

The main advantage of Excel is that it is free and that you can solve all your specific tasks. Of course, you will need to ensure the safety of this file and backup. Also, the use of Excel will allow you to better understand the nuances and subtleties of the movement of money and their accounting.

Currently, Excel's main drawback – accessibility – has been resolved. You can keep a budget in Google Sheets or MS Excel and have full access to the file from any device and anywhere, even without Internet access.

Of course, when creating a basic budget form, you will need certain knowledge and skills in working with these programs. Fortunately, there is the Internet, and it facilitates the solution of this task. But you can use the knowledge gained in your professional field, for example, in work.

We take into account the old fashioned way – a notebook or a notebook

Keeping a budget in a notebook or notepad is less convenient. Since, in addition to fixing your expenses and income, you will need to periodically spend time preparing the form (table) of the budget. In addition, it is very difficult to do visual analytics in this family budgeting tool.

The main advantage of this tool is its autonomy, since it does not depend on the availability of electricity and the charge level of your device, as well as the availability of the Internet.

The golden mean or strategy of use

Which tool to use is up to you. The optimal solution may be to use all the tools at once to solve a specific problem.

For example, the main tool can be Excel, where you will bring together all the data at the end of the day or week and plan your budget. You will record your daily expenses in the application. A notebook or notebook will be a backup tool for fixing daily expenses.

You can develop your own algorithm or strategy for using these tools to manage your family budget.

Typical mistakes in the distribution of the family budget

How do most people allocate money in the family budget? Let's take a standard case, which you probably see, if not on the example of your family, then on the example of relatives, friends and acquaintances.

Finally, the time comes to pay the salary. This day is usually “celebrated”, at least by buying all sorts of goodies for the family table, and as a maximum – they arrange walks with friends and trips to entertainment establishments. They also buy gifts and make surprises for children so that they feel like their parents have received a salary.

- Most of the family's funds are spent on meeting needs in the first days after receiving the money earned. Then the spouses find that they have a debt on utility bills that must be closed until all the money is spent, because until the next paycheck, they need money to live and eat.

- The funds are not immediately used to pay off debts. There is not so much money left, and in the future you need to purchase the necessary things and feed the whole family. Spouses are trying to cut their current spending as much as possible. They only have enough money for food, but they also try to save money on it: they buy only the necessary products.

- Funds are spent unevenly throughout the month to meet personal needs. And then an unplanned situation occurs: the refrigerator broke down, guests unexpectedly came or the youngest child fell ill. … In this case, additional spending of money will be needed, and quite significant for the family wallet. And the funds were gone. You have to borrow from friends, get instant loans and take out loans, because of which the financial situation of the family will only worsen, because this leads to huge additional expenses.

- Lack of savings in the family's wallet can lead to the emergence of debt in unexpected situations. As a result, in the coming months, the family budget will suffer again due to the appearance of arrears, as well as payment of interest on loans and borrowings. What if an unplanned situation re-emerges in the near future? The family's debts will only grow, getting out of the financial hole will not be as easy as sliding down there.

How to properly distribute the family budget with loans? Will family members in such a situation be able to get out of poverty and collect reserve savings that will help them earn additional income? Is it possible to save money for buying a car, renovating an apartment or for a summer trip? Unlikely. Therefore, when planning your family's budget, try to avoid the described mistakes.

3 tips on how to manage a family budget with irregular income

Not everyone has a permanent job with stable salary payments. This does not mean at all that you will not be able to distribute the family budget; you just have to pay more attention to it.

- The first method is to calculate the average income for several years, then you should rely on the figure obtained.

- The second option is to allocate yourself a constant salary from the total amount of income – you need to live on it, and add the remainder to your bank account. In difficult times, write off the missing money from the account. But your income will remain the same.

- The third way to distribute funds is to keep two tables at the same time: for profitable and not very profitable months. It's a little tricky, but possible. Here you can fall into the trap and collect loans in anticipation of profit and good times. But if the bad period lasts a little longer, all of your present and future finances will suffer.

We have described the most useful ways to distribute the family budget, find the most suitable one for yourself. Take it as a basis, use it and look for compromises!

Financial mistakes that can lead to divorce

-

Concealment of personal expenses. 2/3 of married couples hide some personal purchases and debts from their partner. The reasons may be different, but sooner or later everything will be revealed and problems cannot be avoided.

-

Lack of savings, financial cushion will sooner or later affect finances. Problems, sudden difficulties with work and other negative events can devastate the family budget and, as a result, spoil family relationships.

-

Attempts to change and control each other. Each person has his own style of handling money: someone knows how to save, and someone wants to spend everything at once. In this case, it is better to immediately find out all the wishes of each other and agree on a plan for maintaining a budget.

-

The desire to impress the people around you with your wealth, to compare yourself with those around you, to try to become like someone else will also have a deplorable effect on the family budget. It is very important to live within your means, and to approach expenses responsibly, relying on your capabilities and desires.

-

It often happens that only one of the spouses works in a family, most often the husband. And this in no way should mean that the wife does not have the right to vote in financial matters. The position “I earn, so I decide” will definitely not lead to anything good.

-

The position that a man is a breadwinner and is obliged to earn more and manage money has long been irrelevant. Finances should be managed by someone who knows how to do it better and for the benefit of all family members.

-

Combining finances into a shared or even mixed budget for couples with different money management styles is not entirely smart. After all, the hobbies and habits of one of the partners can ruin the whole family.

-

According to the study, the worst relationships are those in which mercantilism prevails, so relationships of convenience rarely last long and are even less likely to be happy.

Ways to settle money issues with each other

It doesn't really matter what type of budgeting a family chooses and who makes the main spending decisions. It's great when a couple knows how to negotiate finances, discuss long-term goals and how to achieve them.

-

Having a financial plan. It is necessary to discuss what future spouses see in 5, 10, 15 years (this includes buying a house, a car, education of children, savings and other important goals and dreams). Then draw up a plan for these expenses by months or years and follow it, analyze and, if necessary, change the conditions.

-

If the family does not have a separate budget, you can agree on how much everyone can spend without asking the spouse's permission. Unplanned purchases from one partner can cause significant damage to the entire family budget and undermine trust in a relationship.

-

Building a financial airbag is one of the most important points. This includes savings “for a rainy day”, on which you can live for a certain time if the main source of income suddenly disappears. Large expenses can be unplanned, and you need to be prepared for this.

To create such a “stash” you need to keep track of income and expenses for 2-3 months and calculate your monthly spending. And the size of the financial cushion is calculated according to the formula: the amount of monthly expenses multiplied by the number of “money-free” months. For example, if your monthly expenses are RUB 50,000, and you want to make a stock for 3 months, then you need to save up RUB 150,000. The optimal period for which you should have a stock of money is from 3 to 6 months. -

Financial issues need to be discussed regularly. It's great when spouses can talk openly with each other about new spending, adjust savings goals, set new goals, and allocate spending. It is most convenient to discuss such issues at the end of the month, and at the same time discuss financial plans for the next one.

How to maintain a family budget if the main expenses are constant with irregular income

Not every person works and has a steady income. However, even in such a situation, you can plan a budget, you just have to do it in more detail.

- The first way is to calculate how much you earn (in recent years) and take this amount as a guideline.

- The next technique is to select an amount from your earnings that will be enough for a living. Set aside the rest for an insurance account. If in any of the months the income is small, you simply take the missing money from the account. In this case, the “salary” will be the same.

- Another way to control the expenses of the family budget is to develop 2 tablets: one for months with normal earnings, and the second for when the income is insufficient. It will not be easy to do this, but if you try, everything will work out. The biggest mistake a person makes when in a similar situation is applying for a loan in the hope that income will increase in the future. However, the problem is that if earnings do not increase, then you will give all the money to pay off the interest on the loan.

Final tips on how to reduce family budget expenses

What does the family budget depend on? First of all, on whether you know how to limit your spending. After all, you can save money only when you save.

- Analyze your household spending. Each day, write down how much you earned and how much you spent. By keeping such records, you will be able to understand what you are spending money on. Be honest with yourself and mark all your expenses. After a couple of months, you will be able to see which purchases you can refuse to start saving.

- Make only the purchases you need. Have you been given a salary today? Postpone shopping at the mall. If you have a large sum on hand, you will not hesitate to buy and spend too much. This is exactly what marketers expect. Having received your salary, write a list of the most necessary expenses and go to the supermarket with this list. At the same time, remember about the mandatory costs – paying apartment bills, credit payments, because you will not be able to reduce costs at their expense.

- Write your shopping list before visiting the store. Has it happened to you that instead of the necessary food, you picked up a lot of sweets, chips and other nasty things? To prevent this from happening, go to the supermarket with a list that also shows the amount you can spend. The hardest part is following this list when you find yourself in the store. Don't shop every day. It is best to do this once every 7 days, with the exception of foods that go bad quickly.

- Don't pay with your card. It is best to pay for purchases in cash. It is psychologically easier to spend a large amount that you do not have on hand, especially when you have a credit card with a large limit. It will be more difficult for you to part with paper money, so you will not spend more than you planned.

- Use coupons, discounts. Get a discount card, buy products for a promotion. For example, if you shop in a large supermarket, get a discount or co-branded card. Buy subscriptions to the fitness club immediately for a year, because it will be more profitable, and you can reduce the costs of the family budget.

- Shop in bulk. Go to a wholesale store and buy goods immediately for a month. For example, products that do not spoil for a long time: sugar, flour, washing powder, and so on. You will immediately feel that the expenses of the family budget have decreased.

- Off-season spending. No need to buy clothes and shoes that are in fashion this season. After all, your savings can be half the cost of a coat or boots from a previous collection.

- Order products from online stores. Online shopping will cost you several times less compared to the same products sold in an offline store. Moreover, on the Internet you can buy not only clothes and shoes, but also home appliances and furniture.

- Reduce the cost of paying utility bills. To do this, install metering devices for gas, water. This way you will spend less on rent. It is estimated that we use less water than the utilities estimate.

- Turn off lights and electrical appliances. Turn off your TV or lights when not in use. Why pay for electricity if you don't use an electrical appliance. Moreover, the risk of short-circuiting the wiring can be reduced.

- Save money on medicines. You've probably heard that health workers from pharmacies indicate expensive drugs in their prescriptions for a certain amount. Ask a therapist if it is possible to replace an expensive medicine with a budget analogue? If the provider refuses to answer, search the web for information.

- Save on mobile and Internet charges. Check if your smartphone has connected paid options? Are you sure you need them? If the answer is no, turn them off. Choose a suitable tariff to reduce the costs of the family budget.

- Save up money. Even if you throw small coins into the piggy bank, when the black streak comes, they can be used to buy food, a bus ticket.

- Give up credit products. Before applying for a credit card or loan, think about whether you can do without getting into debt. For example, you should not take out a loan for travel, purchase of shoes, and the like. You will return from your trip, the interest-free period will end and you will have to refund your money. Remember that the economic situation in the country is constantly changing. You are at great risk, because it may happen that you will not be able to repay the loan.

- Save money every month. Have you been given a salary? Set aside 10% in your emergency reserve. This is the optimal amount, you can save it without harming yourself and your family. Usually we spend this same 10% on unnecessary purchases. By regularly saving a small amount, you will be able to save money for travel, and you will not need to apply for a loan.

- Let the accumulated funds bring passive income. Do you have a large amount? Open a bank deposit and you can get interest on this money. You can also buy securities, trade on the stock exchange. Thus, you will both save and provide yourself with passive income.

Sources used and useful links on the topic: https://littleone.com/publication/0-6607-kak-uchityvat-raspredelyat-i-ekonomit-semeynyy-byudzhet https://www.adme.ru/svoboda-sdelaj-sam / finansovaya-instrukciya-dlya-semejnogo -byudzheta-chtoby-ne-ssoritsya-iz-za-deneg-i-sohranit-semyu- 2245515 / https://money.inguru.ru/navigator/stat_planirovanie_semejnogo_byudzheta https: // equity. today / kak-sostavit-semejnyj-byudzhet-tablicy.html https://mamsy.ru/blog/semejnyj-byudzhet-hitrosti-i-sekrety/ https://moi-ipodom.ru/byudzhet-kak-raspredelit-1 .html http://finstroll.ru/semejnyj-byudzhet-kak-pravilno-vesti/ https://Lifehacker.ru/byudzhet-na-mesyac-i-god/ https://www.papabankir.ru/tips/ kak-pravilno-raspredelit-semejnyj-byudzhet / https://www.papabankir.ru/tips/kak-planirovat-rashody-semejnogo-budzheta/

Post source: lastici.ru